Blog & Community Involvement

Each year on April 22 nd , people worldwide celebrate Earth Day , a holiday dedicated to honoring planet Earth and advocating for environmental protection. But how did Earth Day come to be, and what can we do to celebrate and make a positive impact? Let’s explore the holiday's history and explore ways to commemorate it! The History of Earth Day The birth of Earth Day can be traced back to the 1960s when environmental issues were increasingly gaining attention. Concerns about pollution, deforestation, and the impact of human activities on the planet grew, prompting individuals to act. This paved the way for the idea of Earth Day. Inspired by the anti-war movement, Senator Gaylord Nelson envisioned a nationwide grassroots demonstration to raise awareness about environmental issues. On April 22, 1970, the first Earth Day was celebrated in the United States, drawing millions of people from diverse backgrounds to participate in rallies, teach-ins, and various environmental activities. The success of the inaugural Earth Day was huge. It led to the creation of the Environmental Protection Agency (EPA) and the passage of key environmental legislation, including the Clean Air Act , the Clean Water Act , and the Endangered Species Act . Earth Day had evolved into a global movement, inspiring people worldwide to take action to protect the environment. How to Celebrate Earth Day Educate Yourself and Others Take some time to deepen your understanding of environmental issues facing our planet, from climate change and deforestation to plastic pollution and habitat destruction . Explore reputable sources of information, attend educational events, and engage in meaningful conversations with experts and activists online. Share your knowledge with friends, family, and community members to raise awareness and inspire action. Reduce, Reuse, Recycle Welcome sustainability principles into your daily routine by reducing waste, reusing whatever is possible, and recycling materials such as paper, plastic, glass, and metal. Consider adopting eco-friendly practices such as composting organic waste, using reusable shopping bags and water bottles, and opting for minimally packaged products. Encourage others to adopt these practices and support businesses that prioritize sustainability. Connect with Nature Spend time outdoors and connect with the natural world. Whether exploring a local park, hiking through a forest, or sitting in a garden, immersing yourself in nature can help you foster a deeper appreciation for Earth. Take time to observe wildlife, listen to the sounds, and marvel at the ecosystem’s beauty. Try activities such as bird watching, nature photography, or tree planting! Support Environmental Causes Get involved in environmental initiatives and support organizations addressing pressing environmental challenges. Volunteer your time, skills, and resources to participate in conservation projects, clean-up efforts, and advocacy campaigns. Donate to environmental organizations that are making a difference, and use your voice to advocate for policies and practices that promote sustainability and protect the planet. Your actions, whether by signing petitions, contacting elected officials, or joining movements, can help drive positive change at the local, national, and global levels. Related Article: 2024 Hurricane Survival Guide for Central Florida Residents Celebrate Earth Day Every Day While Earth Day is officially celebrated on April 22 nd , it’s important to remember that caring for the planet is an ongoing commitment that requires sustained effort and dedication. Make Earth-Friendly choices year-round and integrate sustainability into all aspects of your life. Encourage others to join you in adopting environmentally conscious habits and advocate for policies and practices that prioritize the health and well-being of the planet. Working together can create a more sustainable world for present and future generations. Conclusion Earth Day is a powerful reminder of our collective responsibility to protect and preserve the planet for future generations. From its humble beginnings as a grassroots movement to its global impact today, Earth Day has inspired millions of people to act and advocate for environmental stewardship. As we celebrate Earth Day each year, let us reflect on our progress and the challenges that lie ahead. We must reaffirm our commitment to caring for the Earth and working together to build a more sustainable and resilient world. After all, there is no backup planet – it’s up to us to care for the one we have!

Floridians: Hurricane season is approaching! If you’re a resident of Central Florida, you must take steps to protect your home, your family, and your assets from potential damage. In addition to preparing your home and stocking up on essentials, it’s crucial for you to review your insurance coverage to ensure you’re adequately protected. Let’s dive into the importance of having the right insurance coverage, learn practical tips for hurricane preparedness, and outline the necessary steps to take in the aftermath of a storm. The Importance of Good Insurance Coverage Protecting your Home: Homeowners insurance typically covers damage caused by wind, rain, and other dangers associated with hurricanes. However, it’s essential to review policy limits and exclusions to ensure adequate coverage for potential damages. With Central Florida being a hurricane-prone region, you should consider purchasing insurance that covers not only property damage but also additional living expenses in case you need to evacuate your home. Flood Insurance: Standard homeowners insurance policies often do not cover flood damage. Given that Central Florida is affected by flooding due to hurricanes, purchasing flood insurance through the National Flood Insurance Program (NFIP) or a private market insurer (salmon website) is crucial for comprehensive protection. Flood insurance policies typically have a 30-day waiting period before coverage takes effect, so it’s important to plan ahead and secure coverage well before hurricane season begins. Windstorm Insurance: Some insurance policies may require separate windstorm coverage, especially in areas prone to high winds and hurricanes. Review policy details to confirm coverage for wind-related damages, such as roof damage, broken windows, and structural issues. It’s also important to understand any deductibles associated with windstorm coverage and how they may impact the cost of repairs after a hurricane. Some Tips to Prepare for Hurricane Season Review your Insurance Policies: Before hurricane season begins, review your homeowners, flood, and windstorm insurance policies to understand coverage limits, deductibles, and exclusions. Consider consulting with an insurance agent to ensure you have adequate protection based on your property’s location and unique risks. Flood Insurance: Document your belongings and their value through photos, videos, or written inventory. This will facilitate the claims process in case of damage or loss during a hurricane. Keep important documents, such as insurance policies, in a waterproof and portable container as part of your emergency preparedness kit. Windstorm Insurance: Take proactive measures to secure your property and minimize potential damage from high winds and flying debris. Reinforce windows and doors with storm shutters, trim trees and shrubs, and secure loose outdoor items. Consider investing in impact-resistant roofing materials and garage door braces for added protection against hurricane winds. Develop an Emergency Plan: Create a family emergency plan that includes evacuation routes, designated meeting points, and contact information for emergency services and loved ones. Stock up on essential supplies, including non-perishable food, water, medications, flashlights, batteries, and first aid supplies. Some steps to take after the hurricane Assess Your Damage Safely: After the hurricane passes, wait until it’s safe to venture outside and inspect your property for damage. Exercise caution when assessing damage and avoid touching downed power lines or entering flooded areas. Take photos or videos of the damage to support your insurance claim and document the extent of damage. Contact your Insurance Provider, if necessary: Report any damage to your insurance company as soon as possible. Provide detailed information about the extent of the damage and follow their instructions for filing a claim. Be prepared to provide your policy number, contact information, and a description of the damage when reporting a claim. Keep records of all communication with your insurance provider, including claim numbers and adjuster information. Mitigate Further Damage: Take immediate steps to prevent further damage to your property, such as covering broken windows, tarping roofs, and drying out water-damaged areas. Keep receipts for materials and services used to mitigate damage, as these expenses may be covered by your insurance policy. Work with reputable contractors and restoration professionals to ensure the repairs are completed safely and effectively. Document Expenses: Keep detailed records of expenses related to hurricane recovery, including temporary accommodations, repairs, and replacements. This information will help support your insurance claim and ensure that you receive fair compensation for your losses. Be sure to submit all relevant documentation to your insurance company in a timely manner and keep copies for your records. Conclusion Make sure you prepare in advance for hurricanes in Central Florida so you can mitigate the financial impact of storm damage and protect your home and family. Remember to stay informed, stay safe, and be proactive in safeguarding your property against the unpredictable forces of nature. With proper planning and preparation, you can weather the storm and come out stronger!

Introduction In regions like Florida, where the risk of flooding is a constant concern, understanding and securing flood insurance is crucial for homeowners. This specialized insurance provides financial protection against damages caused by flooding, a peril not typically covered under standard homeowners insurance policies. Understanding Flood Insurance Definition and Basics Flood insurance is a specific type of property insurance that covers losses to your home and personal property due to flooding. It's crucial to note that standard homeowners insurance does not cover flood damage . Coverage Details A standard flood insurance policy typically includes: Structural Damage : Covers the repair or rebuilding costs for your home's structure. Personal Property : Provides compensation for damaged personal items. Living Expenses : Assists with costs if your home is temporarily uninhabitable. Assessing Flood Risk Risk Factors Key factors influencing flood risk include proximity to water bodies, regional climate patterns, and local topography. Importance of Risk Assessment Proper risk assessment is essential for determining the need and level of flood insurance coverage. Homeowners should use flood maps and risk assessment tools to gauge their property's vulnerability. The Necessity of Flood Insurance Protection Against Flood Damage Flood insurance acts as a safety net, ensuring homeowners can recover from flood-related losses. Case Studies Examples of flood recovery highlight the critical role of flood insurance in post-disaster financial stability. Flood Insurance vs. Homeowners Insurance Comparative Analysis Homeowners insurance covers various property damages but typically excludes flood damage, underscoring the need for a separate flood insurance policy. Misconceptions Clarified Many homeowners mistakenly believe their standard policy covers flood damage, which can lead to significant financial hardship in the event of a flood. Choosing the Right Flood Policy Factors to Consider When selecting a flood insurance policy, homeowners should consider coverage limits, deductibles, and policy exclusions. Policy Types Options range from National Flood Insurance Program (NFIP) policies to those offered by private insurers, each with unique coverage aspects. Financial Implications Cost of Flood Insurance The cost varies based on location, flood risk, and the value of the insured property. Long-term Financial Benefits Investing in flood insurance can prevent devastating financial losses during a flood event. Steps to Acquire Flood Insurance Process Overview To obtain flood insurance, homeowners should: Assess their flood risk. Compare policy options. Choose the policy that best fits their needs. Resources and Assistance FEMA's Flood Map Service Center and insurance advisors can provide guidance in selecting the appropriate policy. Preparing for Flood Events Preventive Measures Homeowners can minimize flood damage through measures like elevating utilities and installing flood barriers. Community Resources Local programs often offer support for flood preparedness and recovery. Conclusion Flood insurance is an indispensable safeguard for homeowners, particularly in flood-prone areas. It ensures financial resilience in the face of potential flood disasters. Next Steps Evaluate your flood insurance needs and take steps to protect your home and financial future.

Introduction Life insurance in Florida is an essential consideration for residents. It's not just about a policy; it's about securing the future for your loved ones. This guide provides a comprehensive look at life insurance options in the Sunshine State, tailored to meet the unique needs of Floridians. Understanding Life Insurance in Florida What is Life Insurance? Life insurance is a contract where an insurer pays a designated beneficiary a sum of money upon the insured person's death, in exchange for premiums paid during their lifetime. Why It's Important in Florida Florida's diverse demographics and unique environmental factors make understanding life insurance particularly important for residents. Types of Life Insurance Policies Term Life Insurance Features : Fixed-term coverage, usually more affordable. Best For : Short-term coverage needs or limited budgets. Whole Life Insurance Advantages : Lifetime coverage with a savings component. Ideal For : Long-term financial planning and wealth accumulation. Universal Life Insurance Flexibility : Adjustable premiums and benefits. Suitable For : Those needing adaptable coverage over time. Assessing Your Coverage Needs Factors to Consider Age and Health : Younger, healthier individuals typically pay lower premiums. Financial Obligations : Consider debts, income replacement, and future expenses like education or retirement. Calculating Coverage Rule of Thumb : 5 to 10 times your annual income. Personalized Assessment : Consult with a financial advisor for tailored advice. Choosing the Right Policy Comparing Providers Research and compare different insurers. Look for financial stability, customer service, and claim settlement ratios. Understanding Policy Terms Read and understand the fine print, including exclusions and riders. Policy Riders and Additional Coverage Common Riders Accidental Death Benefit : Additional payout in case of accidental death. Waiver of Premium : Waives premiums if you become disabled. Tailoring Your Policy Choose riders based on personal circumstances and future concerns. Life Insurance for Different Life Stages Young Adults Focus : Affordable coverage, typically term life insurance. Mid-Life Adjustments : Increase coverage to reflect growing responsibilities and assets. Seniors Considerations : Estate planning, final expenses, and leaving a legacy. Navigating Life Insurance Claims Filing a Claim Understand the process and required documentation. File promptly and follow up regularly. Challenges in Florida Be aware of potential issues like delayed payouts or disputes. Conclusion Life insurance in Florida is a crucial part of financial planning. Understanding the different types of policies and aligning them with your life stage and goals is key to making informed decisions. Next Steps Review your life insurance needs regularly and consult with a professional to ensure your coverage aligns with your changing life circumstances.

I. Introduction In Florida, homeowners are grappling with a growing crisis in the insurance sector. This article explores the "homeowners insurance crisis" in Florida, examining the challenges faced by insurance companies and homeowners alike. We aim to shed light on the roots of this crisis and its impact on the residents of the Sunshine State. II. Understanding the Homeowners Insurance Crisis in Florida The crisis in Florida's homeowners insurance sector is complex and multifaceted. It has evolved over time, leading to the current precarious situation. This section will define the crisis and provide a historical overview. III. Factors Contributing to the Crisis Several key factors have contributed to the crisis: Weather-Related Challenges : Florida's high risk of hurricanes and floods significantly impacts insurance costs and coverage availability. Legal and Litigation Issues : The state's legal environment, including frequent litigation, has put additional pressure on insurance companies. Economic Factors : Rising property values and repair costs further strain the insurance market. IV. The Impact on Insurance Companies Insurance companies in Florida are deeply affected by the crisis: Many have withdrawn from the market due to unsustainable losses. Financial strains and high-risk assessments are commonplace. V. Consequences for Florida Homeowners Homeowners face direct repercussions: Rising Premiums: Insurance costs have skyrocketed, placing a heavy burden on many homeowners. Coverage Challenges: Obtaining comprehensive coverage is increasingly difficult. Case Studies : Real-life examples highlight the struggles faced by homeowners. VI. Legislative and Regulatory Responses The Florida government and regulatory bodies have taken steps to address the crisis: Recent legislative changes aim to stabilize the market. The effectiveness of these measures is a subject of ongoing debate. VII. Strategies for Homeowners Practical advice for homeowners includes: Tips for securing reliable insurance coverage. Strategies for managing insurance costs. Exploring alternative insurance options in Florida. VIII. The Future Outlook Experts predict a challenging road ahead, but there are potential solutions and strategies for market stabilization. IX. Conclusion This crisis requires awareness and proactive measures from homeowners. Understanding the complexities of the insurance market in Florida is crucial. X. Next Steps Stay informed and actively manage your homeowners insurance needs. Seek out resources for further information and assistance on how to protect your peace of mind.

Introduction In recent years, auto insurance rates have seen a notable surge, leaving many policyholders grappling with higher premiums. This trend is not isolated but part of a broader pattern influenced by a variety of factors. Understanding these factors is crucial for consumers looking to navigate the complexities of auto insurance and manage their expenses effectively. Historical Perspective on Auto Insurance Rates Past vs. Present : A look at how auto insurance rates have evolved over the years. Trend Analysis : Comparing current rates with historical data to understand the magnitude of the increase. The Impact of State Regulations State-Specific Laws : How regulations in states like Florida impact insurance rates. Regulatory Changes : Examples of recent legislative changes and their effects on premiums. The Role of Natural Disasters Disaster-Prone Areas : Analysis of the financial burden on insurance companies due to frequent natural disasters. Case Studies : Examining recent natural events and their impact on insurance costs. Traffic Density and Urbanization Increased Accidents : Correlation between higher traffic density and accident rates. Urban Growth : Statistical data showcasing the relationship between urbanization and insurance premiums. Technological Advancements in Vehicles High-Tech Repairs : The cost implications of advanced technology in modern vehicles. Technology Costs : Examples of technologies that increase repair costs. Insurance Fraud and Its Consequences Fraud Impact : How fraudulent activities contribute to rising insurance rates. Fraud Examples : Common fraudulent practices and their effects on the insurance industry. The Influence of Economic Factors Economic Dynamics : The role of inflation and market conditions in insurance rate adjustments. Economic Impact : How different economic scenarios affect insurance premiums. Demographic Changes and Risk Assessment Changing Demographics : The influence of demographic shifts on insurance rates. Risk Models : How new risk assessment models impact insurance costs. The Effect of Healthcare Costs Healthcare and Insurance : The connection between rising healthcare costs and auto insurance premiums. Healthcare Case Studies : Examples showing the impact of healthcare expenses on insurance claims. Conclusion The increase in auto insurance rates is a multifaceted issue influenced by various factors, from state regulations and natural disasters to technological advancements and economic conditions. Understanding these elements is key to making informed decisions about auto insurance. Next Steps Review your auto insurance policy in light of these factors. For more information or assistance...

I. Introduction In Florida, a state with bustling roads and diverse traffic, understanding Uninsured Motorist Coverage is crucial for every driver. This article delves into the importance of this coverage in Florida's unique auto insurance landscape, offering insights for both new and seasoned drivers. II. Understanding Auto Insurance in Florida Florida's distinctive "No-Fault" Auto Insurance System requires drivers to carry Personal Injury Protection (PIP). However, this system has limitations, especially when dealing with uninsured motorists. Mandatory Insurance Requirements : Florida law mandates that drivers have a minimum of $10,000 in PIP and $10,000 in Property Damage Liability (PDL). No-Fault System Nuances : Understanding the nuances of this system is key to comprehending why additional coverage like UM is beneficial. III. What is Uninsured Motorist Coverage? Uninsured Motorist (UM) Coverage is an additional layer of protection that covers you when the at-fault driver lacks adequate insurance. Functionality : It covers medical expenses, lost wages, and other damages when the other party is uninsured or underinsured. Scope of Coverage : This coverage extends to hit-and-run accidents and instances where the at-fault driver's insurance is insufficient. IV. The Prevalence of Uninsured Drivers in Florida Florida's rate of uninsured drivers, hovering around 20%, is among the highest in the United States, making UM coverage more of a necessity than a luxury. V. Benefits of Uninsured Motorist Coverage UM Coverage offers not just financial protection but also peace of mind in a state with a high rate of uninsured drivers. Comprehensive Protection : It fills the gaps left by PIP and liability coverage, especially in severe accidents. Flexibility and Peace of Mind : Knowing you're covered regardless of the other driver's insurance status provides immense relief. VI. How to Choose the Right Uninsured Motorist Coverage Selecting the right UM Coverage involves a careful assessment of your driving habits, frequent travel areas, and financial situation. Coverage Limits : Understanding how these limits work in conjunction with your PIP and liability coverage is crucial. Cost-Benefit Analysis : Weighing the cost of additional coverage against the potential financial risk of an accident with an uninsured driver. VII. Legal Aspects of Uninsured Motorist Coverage Understanding how UM Coverage complements your PIP and liability coverage under Florida's no-fault system is essential for legal and financial protection. Legal Requirements and Options : While UM coverage is optional, it's often recommended by legal and insurance experts. Policyholder Rights : Knowing your rights under your UM policy can be crucial in the event of an accident. VIII. Dealing with a Car Accident Involving an Uninsured Driver In an accident with an uninsured driver, it's important to document the accident thoroughly, gather witness statements, file a police report, and report the incident to your insurer. Immediate Steps : Safety first, then documentation and reporting. Long-Term Considerations : Understanding how such an accident can impact your future insurance premiums and coverage. IX. Pros and Cons of Uninsured Motorist Coverage While UM Coverage offers enhanced protection, it also adds an additional cost to your insurance premium. However, the benefits often outweigh the costs, especially in a high-risk state like Florida. Pros : Enhanced protection, peace of mind, coverage in hit-and-run scenarios. Cons : Additional cost, potential for underutilization. X. Conclusion Uninsured Motorist Coverage is a critical part of a comprehensive auto insurance plan in Florida. It provides essential protection against the unforeseen and ensures that you are covered in a variety of scenarios, including those involving uninsured or underinsured drivers. XI. Next Steps Review your auto insurance policy to ensure you have adequate coverage. Contact your insurance provider for more information or to adjust your policy. Being proactive can save you from significant financial and legal headaches in the future.

I. Introduction In Florida, a state with bustling roads and diverse traffic, understanding Uninsured Motorist Coverage is crucial for every driver. This article delves into the importance of this coverage in Florida's unique auto insurance landscape, offering insights for both new and seasoned drivers. II. Understanding Auto Insurance in Florida Florida's distinctive "No-Fault" Auto Insurance System requires drivers to carry Personal Injury Protection (PIP). However, this system has limitations, especially when dealing with uninsured motorists. Mandatory Insurance Requirements : Florida law mandates that drivers have a minimum of $10,000 in PIP and $10,000 in Property Damage Liability (PDL). No-Fault System Nuances : Understanding the nuances of this system is key to comprehending why additional coverage like UM is beneficial. III. What is Uninsured Motorist Coverage? Uninsured Motorist (UM) Coverage is an additional layer of protection that covers you when the at-fault driver lacks adequate insurance. Functionality : It covers medical expenses, lost wages, and other damages when the other party is uninsured or underinsured. Scope of Coverage : This coverage extends to hit-and-run accidents and instances where the at-fault driver's insurance is insufficient. IV. The Prevalence of Uninsured Drivers in Florida Florida's rate of uninsured drivers, hovering around 20%, is among the highest in the United States, making UM coverage more of a necessity than a luxury. V. Benefits of Uninsured Motorist Coverage UM Coverage offers not just financial protection but also peace of mind in a state with a high rate of uninsured drivers. Comprehensive Protection : It fills the gaps left by PIP and liability coverage, especially in severe accidents. Flexibility and Peace of Mind : Knowing you're covered regardless of the other driver's insurance status provides immense relief. VI. How to Choose the Right Uninsured Motorist Coverage Selecting the right UM Coverage involves a careful assessment of your driving habits, frequent travel areas, and financial situation. Coverage Limits : Understanding how these limits work in conjunction with your PIP and liability coverage is crucial. Cost-Benefit Analysis : Weighing the cost of additional coverage against the potential financial risk of an accident with an uninsured driver. VII. Legal Aspects of Uninsured Motorist Coverage Understanding how UM Coverage complements your PIP and liability coverage under Florida's no-fault system is essential for legal and financial protection. Legal Requirements and Options : While UM coverage is optional, it's often recommended by legal and insurance experts. Policyholder Rights : Knowing your rights under your UM policy can be crucial in the event of an accident. VIII. Dealing with a Car Accident Involving an Uninsured Driver In an accident with an uninsured driver, it's important to document the accident thoroughly, gather witness statements, file a police report, and report the incident to your insurer. Immediate Steps : Safety first, then documentation and reporting. Long-Term Considerations : Understanding how such an accident can impact your future insurance premiums and coverage. IX. Pros and Cons of Uninsured Motorist Coverage While UM Coverage offers enhanced protection, it also adds an additional cost to your insurance premium. However, the benefits often outweigh the costs, especially in a high-risk state like Florida. Pros : Enhanced protection, peace of mind, coverage in hit-and-run scenarios. Cons : Additional cost, potential for underutilization. X. Conclusion Uninsured Motorist Coverage is a critical part of a comprehensive auto insurance plan in Florida. It provides essential protection against the unforeseen and ensures that you are covered in a variety of scenarios, including those involving uninsured or underinsured drivers. XI. Next Steps Review your auto insurance policy to ensure you have adequate coverage. Contact your insurance provider for more information or to adjust your policy. Being proactive can save you from significant financial and legal headaches in the future.

Introduction In today's insurance landscape, credit-based insurance scores are crucial in determining your insurance premiums. Understanding and improving these scores can lead to more favorable insurance rates. This article explores what these scores are, their significance, and practical tips to enhance them. Understanding Credit-Based Insurance Scores What is a Credit-Based Insurance Score? A credit-based insurance score is a metric used by insurers to assess the risk of insuring an individual. It's similar to a credit score but tailored for the insurance industry. Differences from Regular Credit Scores While both scores are based on financial history, the insurance score focuses more on predicting the likelihood of an insurance claim. Role in Insurance These scores help insurers determine policy pricing, influencing how much you pay for your insurance. Factors Affecting Your Credit-Based Insurance Score Credit History: A record of your financial reliability. Payment Records: Timeliness of your bill payments. Outstanding Debts: The amount of debt you currently owe. Tips to Improve Your Credit-Based Insurance Score Tip 1: Regularly Check Your Credit Report Monitor Your Report: Regularly reviewing your credit report can help you spot errors and areas for improvement. Accessing Your Report: You're entitled to a free credit report annually from each of the three major credit bureaus. Tip 2: Pay Bills on Time Timely Payments: Consistently paying bills on time positively impacts your score. Automated Payments: Setting up automatic payments can ensure you never miss a due date. Tip 3: Reduce Outstanding Debt Debt Management: Actively work to pay down existing debts. Credit Utilization: Aim to use less than 30% of your available credit. Tip 4: Avoid Opening Multiple New Credit Accounts New Accounts: Each new account can temporarily lower your score. Credit Inquiries: Apply for new credit sparingly to avoid multiple hard inquiries. Long-Term Strategies for a Healthy Credit-Based Insurance Score Solid Credit History: Building a strong credit history over time is key. Financial Planning: Effective budgeting and financial planning are essential. Update Personal Information: Keep your information current with credit bureaus. Common Myths and Misconceptions Myth 1: Checking your credit report harms your score. Myth 2: Your income affects your credit-based insurance score. When and How to Seek Professional Advice Professional Financial Advice: Consider consulting a financial advisor for personalized guidance. Choosing an Advisor: Look for reputable advisors with proven expertise. Conclusion Improving your credit-based insurance score is a proactive step towards better financial health. By following these tips and strategies, you can positively influence your insurance premiums. Next Steps Start implementing these tips today to see a difference in your credit-based insurance score. For more information and resources, explore our comprehensive guides on credit and financial management.

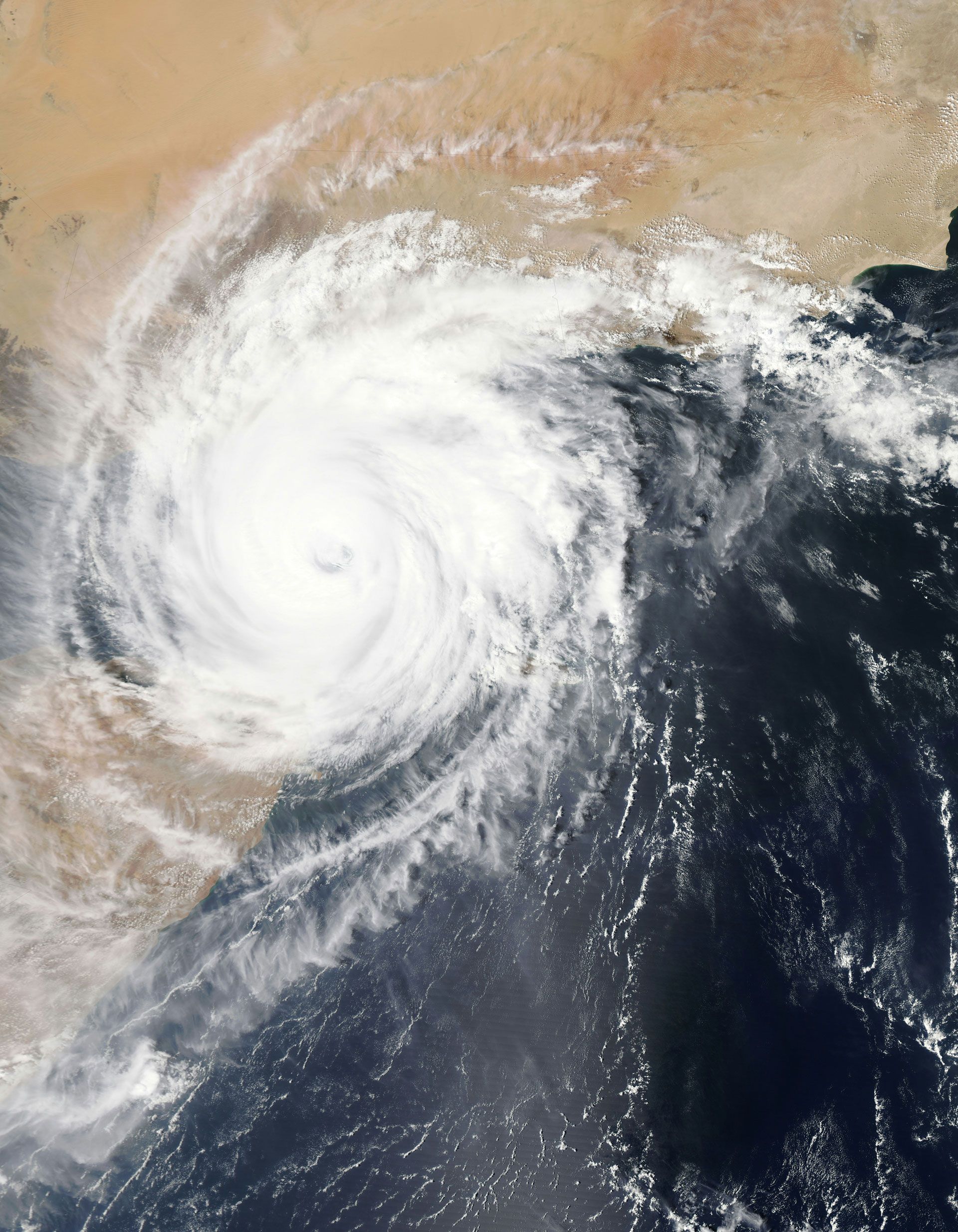

I. Introduction As the hurricane season approaches, it's crucial to understand the importance of being prepared. Each year, these powerful storms pose a significant threat, especially to coastal and low-lying areas. This guide aims to provide you with comprehensive information and practical tips to ensure you and your family are well-prepared for the hurricane season. II. Understanding Hurricane Season What is the Hurricane Season? The hurricane season typically runs from June to November. Historical Data: Analysis of past hurricane patterns, focusing on frequency and intensity. III. The Science Behind Hurricanes Understanding Hurricanes: Formation and development of hurricanes. Hurricane Categories: Explaining categories 1 through 5 and their potential impacts. IV. Preparing Before the Hurricane Season Preparation Checklist: Home fortification tips: Storm shutters, reinforced roofs, and flood barriers. Safety measures: Secure loose outdoor items, trim trees, and check drainage systems. V. Emergency Kits and Supplies Essential Items for Your Kit: Water, non-perishable food, first-aid supplies, flashlights, and batteries. Special Needs: Medications, baby supplies, and pet needs. VI. Evacuation Plans and Routes Effective Evacuation Strategies: Plan multiple evacuation routes. Stay Informed: Keep updated with local authorities about safe evacuation routes. VII. Understanding and Monitoring Hurricane Alerts Staying Informed: Types of alerts: Watches and warnings. Resources: NOAA Weather Radio, local news, and weather apps. VIII. Insurance and Financial Preparedness Insurance Review: Ensure adequate coverage for hurricanes, including flood insurance. Document Safety: Secure important financial documents in waterproof containers. IX. Special Considerations for Pets and Vulnerable Family Members Caring for the Vulnerable: Plan for the safety of pets: Pet-friendly shelters and emergency kits. Vulnerable Individuals: Prepare for the needs of the elderly and those with medical conditions. X. Post-Hurricane Safety and Recovery After the Storm: Safety checks: Avoid floodwaters, watch for downed power lines. Damage Assessment: Document property damage for insurance claims. XI. Community Resources and Support Local Support: Accessing community resources for aid and support. Community Involvement: How to help and where to find help. XII. Building Resilience Against Future Hurricanes Long-Term Strategies: Investing in stronger building materials and designs. Environmental Considerations: Supporting coastal restoration and flood prevention initiatives. XIII. Conclusion Hurricane preparedness is not just about immediate safety; it's about building resilience for the future. By staying informed, planning ahead, and understanding the risks, you can significantly reduce the impact of hurricanes on your life. XIV. Next Steps Share your hurricane preparedness tips and experiences. For more resources and information, visit NOAA's Hurricane Preparedness website and stay connected with your local community for support.