Find The Best Homeowners Insurance For You

Introduction to Insurance Coverage

Homeowners insurance is more than just a contractual necessity; it's a critical component in protecting your most valuable asset – your home. Whether you're a new homeowner or have been settled in your abode for years, understanding how and when to change your homeowners insurance can be as crucial as the policy itself. Homeowners insurance provides essential coverage for your home and assets, helping to protect against damage and financial loss.

In this comprehensive guide, we'll delve into the nuances of changing your home insurance. From knowing why and when to switch, to navigating the complexities of the process, we aim to equip you with all the information you need to make an informed decision.

Why might you consider changing your homeowners insurance?

Perhaps you've found a policy that offers better coverage at a more affordable rate, or maybe your current policy no longer aligns with your evolving needs. Whatever the reason, changing your homeowners insurance and coverage may be a smart financial move, potentially saving you money and enhancing your coverage.

But how do you embark on this journey without getting lost in a maze of insurance jargon and complex procedures? That's where this guide comes in. We'll walk you through each step, ensuring you have a clear roadmap from start to finish.

Stay tuned as we explore the ins and outs of changing your homeowners insurance, and discover how this change can benefit you both financially and in terms of peace of mind.

Understanding Homeowners Insurance

Before diving into the process of changing your policy, it's essential to have a solid understanding of what homeowners insurance is and why it's so important. Homeowners insurance is a form of property insurance that covers losses and damages to an individual's house and assets in the home. It also provides liability coverage against accidents in the home or on the property. This insurance cover is vital in safeguarding your investment and ensuring that you can repair your home in the event of unforeseen damage.

Key Components of Homeowners Coverage:

- Dwelling Coverage: Provides coverage that protects the structure of your home from perils like fire, wind, or hail.

- Personal Property: Covers the loss or damage of home and personal belongings inside the home.

- Liability Protection: Offers coverage if someone is injured on your property and you are deemed legally responsible.

- Additional Living Expenses (ALE): Helps cover the costs of living elsewhere if your home is uninhabitable due to a covered loss.

Understanding these components is crucial as they form the basis of what you'll be comparing when looking at new insurance options.

Reasons to Consider Changing Your Homeowners Insurance

There are several reasons why you might want to change your homeowners insurance provider:

- Finding a Better Rate: If you discover another insurer offers the same coverage at a lower price.

- Changes in Needs: Your current policy may no longer suit your evolving needs.

- Poor Customer Service Experience: Service quality is as important as the coverage itself.

- Bundling Opportunities: Some insurers offer homeowners insurance discounts if you bundle homeowners with other types of insurance, like car insurance or a flood insurance policy.

- Improved Coverage Options: Seeking better or more comprehensive coverage than your current policy offers.

Benefits of Switching: Changing your policy can lead to cost savings, better coverage, and improved customer service.

Best Time to Switch Homeowners Insurance

Timing is key when it comes to changing your homeowners insurance. Here are some ideal times to consider making a switch:

- Policy Renewal Period: This is often the most convenient time to switch, as it avoids potential cancellation fees.

- After Significant Life Changes: Such as buying new valuable items, home renovations, or changes in your family situation.

- If You Find a Better Deal: Sometimes, the savings or improved coverage offered by another insurer might be worth switching before your current policy term ends. Get a free home insurance quote online or quote today from multiple homeowners insurance companies in your area.

Step-by-Step Guide to Changing Your Homeowners Insurance

Changing your homeowners insurance can seem daunting, but breaking it down into steps makes the process manageable.

1. Review Your Current Policy

- Understand your current coverage and note any gaps or excesses.

- Check for any penalties or fees for early cancellation.

2. Assess Your Insurance Needs

- Consider any changes in your life or property that might affect your needs.

- Value of Your Home: Consider the market value of your home and the cost to rebuild your home, as these can influence the amount of coverage you need if your home is damaged. Decide on the type and amount of homeowners insurance coverage you need to protect your home and belongings.

- Location of Your Home: The geographical location can affect your insurance rates and requirements, especially if you're in an area prone to certain natural disasters.

- Condition of Your Home: A home inspection might reveal aspects of your home that could impact your insurance, such as the need for repairs or updates.

3. Research and Compare Other Home Insurance Companies

- Look for insurers with strong financial ratings and positive customer reviews.

- Consider both national and local insurance companies.

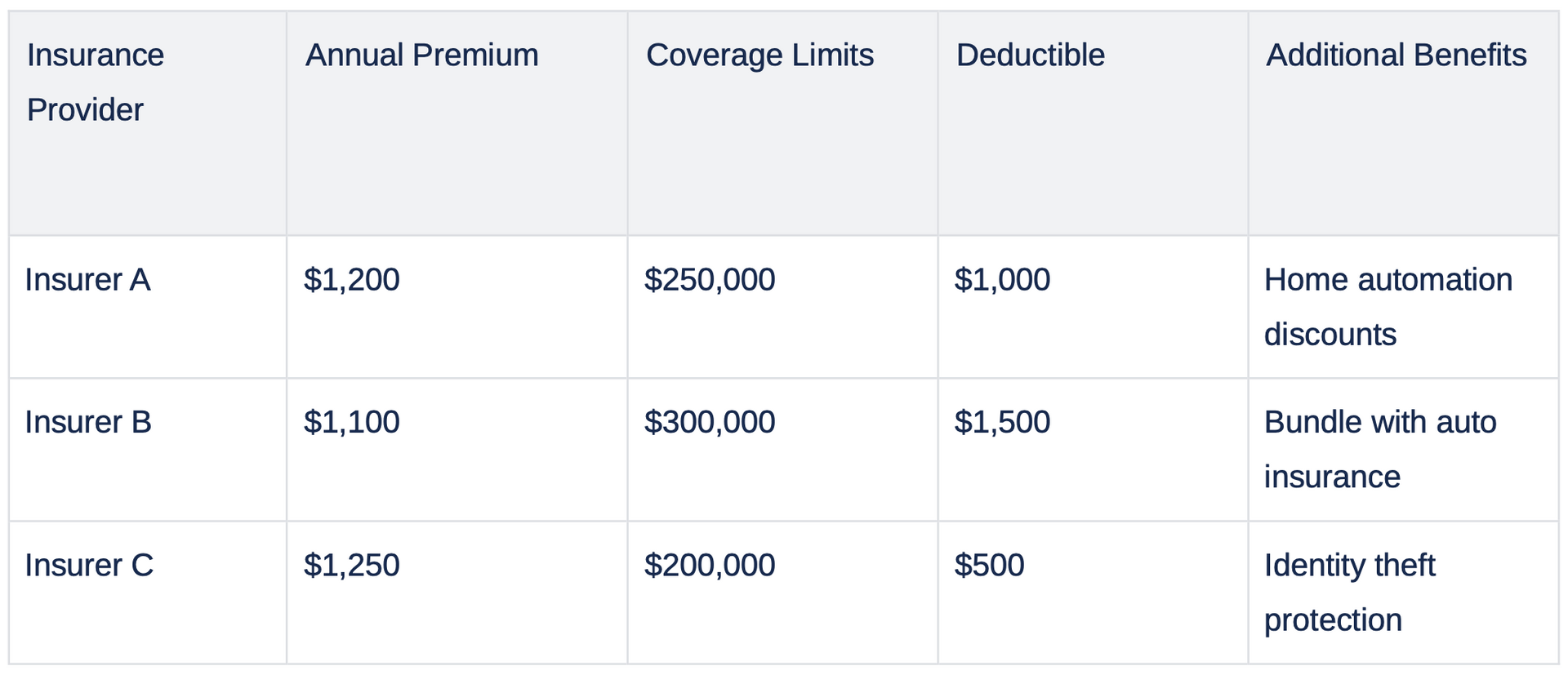

4. Get Home Insurance Quotes and Compare Prices

- Get a quote for similar coverage from multiple homeowners insurance companies.

- Use a table to compare the key features and prices of each quote.

5. Consider the Impact on Your Mortgage

- If you have a mortgage, your lender may have specific requirements for your homeowners insurance.

6. Make the Switch

- Once you've chosen a new insurer, contact them to start the policy.

- Ensure there's no gap in coverage during the transition.

7. Notify Your Mortgage Lender (if applicable)

- Inform your lender about the change in your insurance provider.

Tips for a Smooth Transition

- Avoid Coverage Gaps: Ensure your new policy starts the day after your old policy ends.

- Read the Fine Print: Understand the terms and conditions of your new policy.

- Use an Insurance Agent: They can help streamline the process and find the best deal for you.

Common Home Insurance Mistakes to Avoid

- Not Comparing Enough Options: Always get multiple quotes, as home insurance policies can have subtle differences.

- Overlooking Coverage Details: Don't sacrifice important coverage for a lower price.

- Forgetting to Inform Your Mortgage Lender: This can lead to complications, especially if your insurance is escrowed.

Common Homeowners Insurance Questions

1. Can

I change my homeowners insurance anytime?

- Yes, but consider potential cancellation fees and coverage gaps.

2. Will changing my insurance affect my mortgage?

- It shouldn't, as long as you meet your lender's insurance requirements.

3. How do I know if I'm getting a good deal?

- Compare additional coverage details, not just prices, and read customer reviews.

- Get a free quote and ask about insurance discounts

Conclusion

Changing your homeowners insurance can be a wise financial decision, offering potential savings and better coverage. By following the steps outlined in this guide, you can navigate the process with confidence and ease.

Next Steps

If you're considering changing your homeowners insurance and need more personalized advice, don't hesitate to reach out for expert guidance. Remember, not all homeowners policies are the same. The right insurance policy is one that meets your unique needs and provides peace of mind.

Get a homeowners quote online today and start protecting your home and future.